Aug 29, 2021 | Uncategorized

Computing and Interpreting the Fixed Asset Turnover Ratio from a Financial Analyst’s Perspective The following data were included in a recent Apple Inc. annual report ($ in millions):

|

In millions

|

2006

|

2007

|

2008

|

2009

|

|

Net sales

|

$19,315

|

$24,006

|

$32,479

|

$36,537

|

|

Net property, plant, and equipment

|

1,281

|

1,832

|

2,954

|

2,455

|

Required:

1. Compute Apple’s fixed asset turnover ratio for 2007, 2008, and 2009.

2. How might a financial analyst interpret the results?

Aug 29, 2021 | Uncategorized

Computing and Recording Cost and Depreciation of Assets (Straight Line Depreciation) K Delta Company bought a building for $71,000 cash and the land on which it was located for $107,000 cash. The company paid transfer costs of $9,000 ($3,000 for the building and $6,000 for the land). Renovation costs on the building were $23,000.

Required:

1. Give the journal entry to record the purchase of the property, including all expenditures. Assume that all transactions were for cash and that all purchases occurred at the start of the year.

2. Compute straight line depreciation at the end of one year, assuming an estimated 10 year useful life and a $15,000 estimated residual value.

3. What would be the net book value of the property (land and building) at the end of year 2?

Aug 29, 2021 | Uncategorized

Determining Financial Statement Effects of an Asset Acquisition and Depreciation (Straight Line Depreciation) Ashkar Company ordered a machine on January 1, 2012, at an invoice price of $21,000. On the date of delivery, January 2, 2012, the company paid $6,000 on the machine, with the balance on credit at 10 percent interest. On January 3, 2012, it paid $1,000 for freight on the machine. On January 5, Ashkar paid installation costs relating to the machine amounting to $2,500. On July 1, 2012, the company paid the balance due on the machine plus the interest. On December 31, 2012 (the end of the accounting period), Ashkar recorded depreciation on the machine using the straight line method with an estimated useful life of 10 years and an estimated residual value of $4,000.

Required (round all amounts to the nearest dollar):

1. Indicate the effects (accounts, amounts, and + or ) of each transaction (on January 1, 2, 3, and 5 and July 1) on the accounting equation. Use the following schedule:

Date Assets = Liabilities + Stockholders’ Equity

2. Compute the acquisition cost of the machine.

3. Compute the depreciation expense to be reported for 2012.

4. What impact does the interest paid on the 10 percent note have on the cost of the machine? Under what circumstances can interest expense be included in acquisition cost?

5. What would be the net book value of the machine at the end of 2013?

Aug 29, 2021 | Uncategorized

Recording Depreciation and Repairs (Straight Line Depreciation) – Nasoff Company operates a small manufacturing facility as a supplement to its regular service activities. At the beginning of 2011, an asset account for the company showed the following balances:

|

Manufacturing equipment

|

$100,000

|

|

Accumulated depreciation through 2010

|

54,000

|

During 2011, the following expenditures were incurred for the equipment:

|

Routine maintenance and repairs on the equipment

|

$1,000

|

|

Major overhaul of the equipment that improved efficiency on January 2, 2011

|

12,000

|

The equipment is being depreciated on a straight line basis over an estimated life of 15 years with a $10,000 estimated residual value. The annual accounting period ends on December 31.

Required:

1. Give the adjusting entry that was made at the end of 2010 for depreciation on the manufacturing equipment.

2. Starting at the beginning of 2011, what is the remaining estimated life?

3. Give the journal entries to record the two expenditures during 2011.

Aug 29, 2021 | Uncategorized

Computing Depreciation under Alternative Methods Sterling Steel Inc. purchased a new stamping machine at the beginning of the year at a cost of $580,000. The estimated residual value was $60,000. Assume that the estimated useful life was five years, and the estimated productive life of the machine was 260,000 units. Actual annual production was as follows:

|

Year

|

Units

|

|

1

|

73,000

|

|

2

|

62,000

|

|

3

|

30,000

|

|

4

|

53,000

|

|

5

|

42,000

|

Required:

1. Complete a separate depreciation schedule for each of the alternative methods. Round your answers to the nearest dollar.

a. Straight line.

b. Units of production.

c. Double declining balance.

|

Method:

|

|

Year

|

Computation

|

Depreciation Expense

|

Accumulated Depreciation

|

Net Book Value

|

|

At acquisition

|

|

1

|

|

2

|

|

2. Assuming that the machine was used directly in the production of one of the products that the company manufactures and sells, what factors might management consider in selecting a preferable depreciation method in conformity with the matching principle?

Aug 29, 2021 | Uncategorized

Computing Depreciation and Book Value for Two Years Using Alternative Depreciation Methods and Interpreting the Impact on Cash Flows – Schrade Company bought a machine for $96,000 cash. The estimated useful life was four years, and the estimated residual value was $6,000. Assume that the estimated useful life in productive units is 120,000. Units actually produced were 43,000 in year 1 and 45,000 in year 2.

Required:

1. Determine the appropriate amounts to complete the following schedule. Show computations, and round to the nearest dollar.

|

Depreciation Expense for

|

Net Book Value at the End of

|

|

Method of Depreciation

|

Year 1

|

Year 2

|

Year 1

|

Year 2

|

|

Straight line

|

|

Units of production

|

|

Double declining balance

|

2. Which method would result in the lowest EPS for year 1? For year 2?

3. Which method would result in the highest amount of cash outflows in year 1? Why?

4. Indicate the effects of ( a ) acquiring the machine and ( b ) recording annual depreciation on the operating and investing activities sections of the statement of cash flows (indirect method) for year 1 (assume the straight line method).

Aug 29, 2021 | Uncategorized

Recording the Disposal of an Asset at Three Different Sale Prices FedEx is the world’s leading express distribution company. In addition to the world’s largest fleet of allcargo aircraft, the company has more than 654 aircraft and 51,000 vehicles and trailers that pick up and deliver packages. Assume that FedEx sold a delivery truck that had been used in the business for three years. The records of the company reflected the following:

|

Delivery truck cost

|

$38,000

|

|

Accumulated depreciation

|

23,000

|

Required:

1. Give the journal entry for the disposal of the truck, assuming that the truck sold for

a. $15,000 cash

b. $15,600 cash

c. $14,600 cash

2. Based on the three preceding situations, explain the effects of the disposal of an asset.

Aug 29, 2021 | Uncategorized

Recording the Disposal of an Asset at Three Different Sale Prices – Marriott International is a worldwide operator and franchisor of hotels and related lodging facilities totaling over $1.4 billion in property and equipment. It also develops, operates, and markets time share properties totaling nearly $2 billion. Assume that Marriott replaced furniture that had been used in the business for five years. The records of the company reflected the following regarding the sale of the existing furniture:

|

Furniture (cost)

|

$6,000,000

|

|

Accumulated depreciation

|

5,500,000

|

Required:

1. Give the journal entry for the disposal of the furniture, assuming that it was sold for

a. $500,000 cash

b. $1,600,000 cash

c. $400,000 cash

2. Based on the three preceding situations, explain the effects of the disposal of an asset.

Aug 29, 2021 | Uncategorized

Inferring Asset Age and Recording Accidental Loss on a Long Lived Asset (Straight Line Depreciation) On January 1, 2012, the records of Seward Corporation showed the following regarding a truck:

|

Equipment (estimated residual value, $8,000)

|

$18,000

|

|

Accumulated depreciation (straight line, three years)

|

6,000

|

On December 31, 2012, the delivery truck was a total loss as the result of an accident.

Required:

1. Based on the data given, compute the estimated useful life of the truck.

2. Give all journal entries with respect to the truck on December 31, 2012. Show computations.

Aug 29, 2021 | Uncategorized

Computing the Acquisition and Depletion of a Natural Resource Freeport McMoRan Copper & Gold Inc., headquartered in Phoenix, Arizona, is one of the world’s largest copper, gold, and molybdenum mining and production companies, with its principal asset in natural resource reserves (approximately 102.0 billion pounds of copper, 40.0 million ounces of gold, 2.48 billion pounds of molybdenum, 266.6 million ounces of silver, and 0.7 billion pounds of cobalt, as of the end of 2008). Its annual revenues exceed $17.7 billion. Assume that in February 2012, Freeport McMoRan paid $700,000 for a mineral deposit in Indonesia.

During March, it spent $74,000 in preparing the deposit for exploitation. It was estimated that 900,000 total cubic yards could be extracted economically. During 2012, 60,000 cubic yards were extracted. During January 2013, the company spent another $6,000 for additional developmental work that increased the estimated productive capacity of the mineral deposit.

Required:

1. Compute the acquisition cost of the deposit in 2012.

2. Compute depletion for 2012.

3. Compute the net book value of the deposit after payment of the January 2013 developmental costs.

Aug 29, 2021 | Uncategorized

Computing and Reporting the Acquisition and Amortization of Three Different Intangible Assets Trotman Company had three intangible assets at the end of 2012 (end of the accounting year):

a. Computer software and Web development technology purchased on January 1, 2011, for $70,000. The technology is expected to have a four year useful life to the company.

b. A patent purchased from Ian Zimmer on January 1, 2012, for a cash cost of $6,000. Zimmer had registered the patent with the U.S. Patent Office five years ago.

c. An internally developed trademark registered with the federal government for $13,000 on November 1, 2012. Management decided the trademark has an indefinite life.

Required:

1. Compute the acquisition cost of each intangible asset.

2. Compute the amortization of each intangible at December 31, 2012. The company does not use contra accounts.

3. Show how these assets and any related expenses should be reported on the balance sheet and income statement for 2012.

Aug 29, 2021 | Uncategorized

Computing and Reporting the Acquisition and Amortization of Three Different Intangible Assets Cheshire Company had three intangible assets at the end of 2011 (end of the accounting year):

a. A copyright purchased on January 1, 2011, for a cash cost of $12,300. The copyright is expected to have a 10 year useful life to Cheshire.

b. Goodwill of $65,000 from the purchase of the Hartford Company on July 1, 2010.

c. A patent purchased on January 1, 2010, for $39,200. The inventor had registered the patent with the U.S. Patent Office on January 1, 2006.

Required:

1. Compute the acquisition cost of each intangible asset.

2. Compute the amortization of each intangible at December 31, 2011. The company does not use contra accounts.

3. Show how these assets and any related expenses should be reported on the balance sheet and income statement for 2011. (Assume there has been no impairment of goodwill.)

Aug 29, 2021 | Uncategorized

Recording Leasehold Improvements and Related Amortization – Starbucks Corporation is the leading roaster and retailer of specialty coffee, with nearly 17,000 company operated and licensed stores worldwide. Assume that Starbucks planned to open a new store on Commonwealth Avenue near Boston University and obtained a 10 year lease starting January 1, 2012. The company had to renovate the facility by installing an elevator costing $375,000. Amounts spent to enhance leased property are capitalized as intangible assets called Leasehold Improvements. The elevator will be amortized over the useful life of the lease.

Required:

1. Give the journal entry to record the installation of the new elevator.

2. Give any adjusting entries required at the end of the annual accounting period on December 31, 2012, related to the new elevator. Show computations.

Aug 29, 2021 | Uncategorized

Finding Financial Information as a Potential Investor You are considering investing the cash gifts you received for graduation in various stocks. You have received several annual reports of major companies.

Required:

For each of the following, indicate where you would locate the information in an annual report.

1. Depreciation expense.

2. The detail on major classifications of long lived assets.

3. Prior year’s accumulated depreciation.

4. The accounting method(s) used for financial reporting purposes.

5. Net amount of property, plant, and equipment.

6. Whether the company has had any capital expenditures for the year.

7. Policies on amortizing intangibles.

8. Any significant gains or losses on disposals of fixed assets.

9. The amount of assets written off as impaired during the year.

Recording a Change in Estimate

Required:

Give the adjusting entry that should be made by Nasoff Company at the end of 2011 for depreciation of the manufacturing equipment, assuming no change in the original estimated life or residual value. Show computations.

Aug 29, 2021 | Uncategorized

Recording and Explaining Depreciation, Extraordinary Repairs, and Changes in Estimated Useful Life and Residual Value (Straight Line Depreciation) – At the end of the annual accounting period, December 31, 2012, O’Connor Company’s records reflected the following for Machine A:

|

Cost when acquired

|

$30,000

|

|

Accumulated depreciation

|

10,200

|

During January 2013, the machine was renovated at a cost of $15,500. As a result, the estimated life increased from five years to eight years, and the residual value increased from $4,500 to $6,500. The company uses straight line depreciation.

Required:

1. Give the journal entry to record the renovation.

2. How old was the machine at the end of 2012?

3. Give the adjusting entry at the end of 2013 to record straight line depreciation for the year.

4. Explain the rationale for your entries in requirements 1 and 3.

Aug 29, 2021 | Uncategorized

Analyzing Notes to Adjust Inventory from LIFO to FIFO The following note was contained in a recent Ford Motor Company annual report:

|

NOTE 8. INVENTORIES—AUTOMOTIVE SECTOR

Inventories at December 31 were as follows (dollars in millions)

|

|

Current Year

|

Previous Year

|

|

Raw material, work in process, & supplies

|

$3,016

|

$4,360

|

|

Finished products

|

6,493

|

6,861

|

|

Total inventories at FIFO

|

9,509

|

11,221

|

|

Less LIFO Adjustment

|

891

|

1,100

|

|

Total

|

$8,618

|

$10,121

|

Required:

1. What amount of ending inventory would have been reported in the current year if Ford had used only FIFO?

2. The cost of goods sold reported by Ford for the current year was $127,103 million. Determine the cost of goods sold that would have been reported if Ford had used only FIFO for both years.

3. Explain why Ford management chose to use LIFO for certain of its inventories.

Aug 29, 2021 | Uncategorized

Analyzing and Interpreting the Impact of an Inventory Error – Grants Corporation prepared the following two income statements (simplified for illustrative purposes):

|

First Quarter 2011

|

Second Quarter 2011

|

|

Sales revenue

|

$11,000

|

$18,000

|

|

Cost of goods sold

|

|

Beginning inventory

|

$4,000

|

$3,800

|

|

Purchases

|

3,000

|

13,000

|

|

Goods available for sale

|

7,000

|

16,800

|

|

Ending inventory

|

3,800

|

9,000

|

|

Cost of goods sold

|

3,200

|

7,800

|

|

Gross profit

|

7,800

|

10,200

|

|

Expenses

|

5,000

|

6,000

|

|

Pretax income

|

$2,800

|

$4,200

|

During the third quarter, it was discovered that the ending inventory for the first quarter should have been $4,400.

Required:

1. What effect did this error have on the combined pretax income of the two quarters? Explain.

2. Did this error affect the EPS amounts for each quarter? Explain.

3. Prepare corrected income statements for each quarter.

4. Set up a schedule with the following headings to reflect the comparative effects of the correct and incorrect amounts on the income statement:

|

1st Quarter

|

2nd Quarter

|

|

Income Statement Item

|

Incorrect

|

Correct

|

Error

|

Incorrect

|

Correct

|

Error

|

Aug 29, 2021 | Uncategorized

Recording Sales and Purchases with Cash Discounts Brett’s Cycles sells merchandise on credit terms of 2/15, n/30. A sale invoiced at $900 (cost of sales $600) was made to Shannon Allen on February 1, 2011. The company uses the gross method of recording sales discounts.

Required:

1. Give the journal entry to record the credit sale. Assume use of the perpetual inventory system.

2. Give the journal entry, assuming that the account was collected in full on February 9, 2011.

3. Give the journal entry, assuming, instead, that the account was collected in full on March 2, 2011.

On March 4, 2011, the company purchased bicycles and accessories from a supplier on credit, invoiced at $8,400; the terms were 3/10, n/30. The company uses the gross method to record purchases.

Required:

4. Give the journal entry to record the purchase on credit. Assume the use of the perpetual inventory system.

5. Give the journal entry, assuming that the account was paid in full on March 12, 2011.

6. Give the journal entry, assuming, instead, that the account was paid in full on March 28, 2011.

Aug 29, 2021 | Uncategorized

Recording Purchases and Sales Using a Perpetual and Periodic Inventory System Misty Company reported beginning inventory of 100 units at a unit cost of $20. It engaged in the following purchase and sale transactions during 2011:

Jan. 14 Sold 20 units at unit sales price of $47.50 on open account.

April 9 Purchased 15 additional units at unit cost of $20 on open account.

Sept. 2 Sold 45 units at sales price of $50 on open account.

At the end of 2011, a physical count showed that Misty Company had 50 units of inventory still on hand.

Required:

Record each transaction, assuming that Misty Company uses ( a ) a perpetual inventory system and ( b ) a periodic inventory system (including any necessary entries at the end of the accounting period on December 31).

Aug 29, 2021 | Uncategorized

Portfolio Expected Returns Calculate the expected return on a portfolio of 40 percent Roll and 60 percent Ross by filling in the following:

|

(1)

|

(2)

|

(3)

|

(4)

|

|

State of

|

Probability of

|

Portfolio Return if State Occurs

|

Product

|

|

the

|

State of the

|

|

(2) × (3)

|

|

Economy

|

Economy

|

|

|

|

|

|

E(RP) =

|

|

Aug 29, 2021 | Uncategorized

Portfolio Returns and Volatilities Given the following information, calculate the expected return and standard deviation for a portfolio that has 40 percent invested in Stock A, 30 percent in Stock B, and the balance in Stock C.

|

State of

|

Probability of

|

|

|

|

|

Economy

|

State of

|

Returns

|

|

Boom

|

Economy

|

Stock A

|

Stock B

|

Stock C

|

|

Bust

|

0.4

|

15%

|

18%

|

20%

|

|

|

0.6

|

5

|

0

|

5

|

Aug 29, 2021 | Uncategorized

Asset Allocation Fill in the missing information assuming a correlation of .10.

|

Portfolio

|

Weights

|

Expected

|

Standard

|

|

Stocks

|

Bonds

|

Return

|

Deviation

|

|

1

|

|

14%

|

20%

|

|

0.8

|

|

|

|

|

0.6

|

|

|

|

|

0.4

|

|

|

|

|

0.2

|

|

|

|

|

0

|

|

5%

|

8%

|

Aug 29, 2021 | Uncategorized

Evaluating the LIFO and FIFO Choice When Costs Are Rising and Falling Income is to be evaluated under four different situations as follows:

a. Prices are rising:

(1) Situation A: FIFO is used.

(2) Situation B: LIFO is used.

b. Prices are falling:

(1) Situation C: FIFO is used.

(2) Situation D: LIFO is used.

The basic data common to all four situations are: sales, 500 units for $15,000; beginning inventory, 300 units; purchases, 400 units; ending inventory, 200 units; and operating expenses, $4,000. The following tabulated income statements for each situation have been set up for analytical purposes:

|

PRICES RISING

|

PRICES FALLING

|

|

Situation A

FIFO

|

Situation B

LIFO

|

Situation C

FIFO

|

Situation D

LIFO

|

|

Sales revenue

|

$15,000

|

$15,000

|

$15,000

|

$15,000

|

|

Cost of goods sold:

|

|

Beginning inventory

|

3,300

|

?

|

?

|

?

|

|

Purchases

|

4,800

|

?

|

?

|

?

|

|

Goods available for sale

|

8,100

|

?

|

?

|

?

|

|

Ending inventory

|

2,400

|

?

|

?

|

?

|

|

Cost of goods sold

|

5,700

|

?

|

?

|

?

|

|

Gross profit

|

9,300

|

?

|

?

|

?

|

|

Expenses

|

4,000

|

4,000

|

4,000

|

4,000

|

|

Pretax income

|

5,300

|

?

|

?

|

?

|

|

Income tax expense (30%)

|

1,590

|

?

|

?

|

?

|

|

Net income

|

$3,710

|

Required:

1. Complete the preceding tabulation for each situation. In Situations A and B (prices rising), assume the following: beginning inventory, 300 units at $11 = $3,300; purchases, 400 units at $12 = $4,800. In Situations C and D (prices falling), assume the opposite; that is, beginning inventory, 300 units at $12 = $3,600; purchases, 400 units at $11 = $4,400. Use periodic inventory procedures.

2. Analyze the relative effects on pretax income and on net income as demonstrated by requirement (1) when prices are rising and when prices are falling.

3. Analyze the relative effects on the cash position for each situation.

4. Would you recommend FIFO or LIFO? Explain.

Aug 29, 2021 | Uncategorized

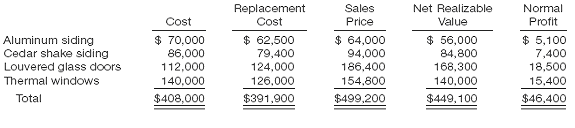

Evaluating the Income Statement and Cash Flow Effects of Lower of Cost or Market Harvey Company prepared its annual financial statements dated December 31, 2011. The company applies the FIFO inventory costing method; however, the company neglected to apply LCM to the ending inventory. The preliminary 2011 income statement follows:

|

Sales revenue

|

$280,000

|

|

Cost of goods sold

|

|

Beginning inventory

|

$33,000

|

|

Purchases

|

184,000

|

|

Goods available for sale

|

217,000

|

|

Ending inventory (FIFO cost)

|

46,500

|

|

Cost of goods sold

|

170,500

|

|

Gross profit

|

109,500

|

|

Operating expenses

|

62,000

|

|

Pretax income

|

47,500

|

|

Income tax expense (30%)

|

14,250

|

|

Net income

|

$33,250

|

Assume that you have been asked to restate the 2011 financial statements to incorporate LCM. You have developed the following data relating to the 2011 ending inventory:

|

Acquisition Cost

|

Current Replacement Unit Cost

|

|

Item

|

Quantity

|

Unit

|

Total

|

(Market)

|

|

A

|

3,050

|

$3

|

$9,150

|

$4

|

|

B

|

1,500

|

5

|

7,500

|

3.5

|

|

C

|

7,100

|

1.5

|

10,650

|

3.5

|

|

D

|

3,200

|

6

|

19,200

|

4

|

|

$46,500

|

Required:

1. Restate this income statement to reflect LCM valuation of the 2011 ending inventory. Apply LCM on an item by item basis and show computations.

2. Compare and explain the LCM effect on each amount that was changed on the income statement in requirement (1).

3. What is the conceptual basis for applying LCM to merchandise inventories?

4. Thought question: What effect did LCM have on the 2011 cash flow? What will be the long term effect on cash flow?

Aug 29, 2021 | Uncategorized

Evaluating the Effects of Manufacturing Changes on Inventory Turnover Ratio and Cash Flows from Operating Activities Carter and Company has been operating for five years as an electronics component manufacturer specializing in cellular phone components. During this period, it has experienced rapid growth in sales revenue and in inventory. Mr. Carter and his associates have hired you as its first corporate controller. You have put into place new purchasing and manufacturing procedures that are expected to reduce inventories by approximately one third by year end. You have gathered the following data related to the changes:

|

(dollars in thousands)

|

|

Beginning of Year

|

End of Year (projected)

|

|

Inventory

|

$595,700

|

$394,310

|

|

Current Year (projected)

|

|

Cost of goods sold

|

$7,008,984

|

Required:

1. Compute the inventory turnover ratio based on two different assumptions:

a. Those presented in the preceding table (a decrease in the balance in inventory).

b. No change from the beginning of the year inventory balance.

2. Compute the effect of the projected change in the balance in inventory on cash flow from operating activities for the year (the sign and amount of effect).

3. On the basis of the preceding analysis, write a brief memo explaining how an increase in inventory turnover can result in an increase in cash flow from operating activities. Also explain how this increase can benefit the company.

Aug 29, 2021 | Uncategorized

Evaluating the Choice between LIFO and FIFO Based on an Inventory Note An annual report for General Motors Corporation included the following note: Inventories are stated generally at cost, which is not in excess of market. The cost of substantially all domestic inventories was determined by the last in, first out (LIFO) method. If the first in, first out (FIFO) method of inventory valuation had been used by the corporation for U.S. inventories, it is estimated that they would be $2,077.1 million higher at the end of this year, compared with $1,784.5 million higher at the end of last year. For the year, GM reported net income (after taxes) of $320.5 million. At year end, the balance of the GM retained earnings account was $15,340 million.

Required:

1. Determine the amount of net income that GM would have reported for the year if it had used the FIFO method (assume a 30 percent tax rate).

2. Determine the amount of retained earnings that GM would have reported at year end if it always had used the FIFO method (assume a 30 percent tax rate).

3. Use of the LIFO method reduced the amount of taxes that GM had to pay for the year compared with the amount that would have been paid if GM had used FIFO. Calculate the amount of this reduction (assume a 30 percent tax rate).

Aug 29, 2021 | Uncategorized

Analyzing and Interpreting the Effects of Inventory Errors The income statement for Pruitt Company summarized for a four year period show the following:

|

2011

|

2012

|

2013

|

2014

|

|

Sales revenue

|

$2,025,000

|

$2,450,000

|

$2,700,000

|

$2,975,000

|

|

Cost of goods sold

|

1,505,000

|

1,627,000

|

1,782,000

|

2,113,000

|

|

Gross profit

|

520,000

|

823,000

|

918,000

|

862,000

|

|

Expenses

|

490,000

|

513,000

|

538,000

|

542,000

|

|

Pretax income

|

30,000

|

310,000

|

380,000

|

320,000

|

|

Income tax expense (30%)

|

9,000

|

93,000

|

114,000

|

96,000

|

|

Net income

|

$21,000

|

$217,000

|

$266,000

|

$224,000

|

An audit revealed that in determining these amounts, the ending inventory for 2012 was overstated by $18,000. The company uses a periodic inventory system.

Required:

1. Recast the income statements to reflect the correct amounts, taking into consideration the inventory error.

2. Compute the gross profit percentage for each year ( a ) before the correction and ( b ) after the correction.

3. What effect would the error have had on the income tax expense assuming a 30 percent average rate?

Aug 29, 2021 | Uncategorized

Analyzing LIFO and FIFO When Inventory Quantities Decline Based on an Actual Note In a recent annual report, General Electric reported the following in its inventory note:

|

December 31 (dollars in millions)

|

Current Year

|

Prior Year

|

|

Raw materials and work in progress

|

$5,603

|

$5,515

|

|

Finished goods

|

2,863

|

2,546

|

|

Unbilled shipments

|

246

|

280

|

|

8,712

|

8,341

|

|

Less revaluation to LIFO

|

2,226

|

2,076

|

|

LIFO value of inventories

|

$6,486

|

$6,265

|

It also reported a $23 million change in cost of goods sold due to “lower inventory levels.”

Required:

1. Compute the increase or decrease in the pretax operating profit (loss) that would have been reported for the current year had GE employed FIFO accounting for all inventory for both years.

2. Compute the increase or decrease in pretax operating profit that would have been reported had GE employed LIFO but not reduced inventory quantities during the current year.

Aug 29, 2021 | Uncategorized

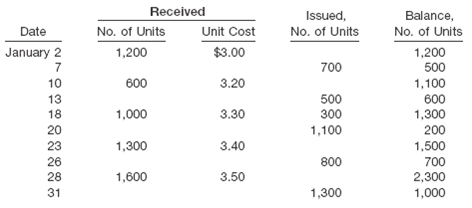

Analyzing the Effects of Four Alternative Inventory Methods – Dixon Company uses a periodic inventory system. At the end of the annual accounting period, December 31, 2011, the accounting records for the most popular item in inventory showed the following:

|

Transactions

|

Units

|

Unit Cost

|

|

Beginning inventory, January 1, 2011

|

390

|

$32

|

|

Transactions during 2011:

|

|

a. Purchase, February 20

|

700

|

34

|

|

b. Purchase, June 30

|

460

|

37

|

|

c. Sale ($50 each)

|

70

|

|

d. Sale ($50 each)

|

750

|

Required:

Compute the cost of ( a ) goods available for sale, ( b ) ending inventory, and ( c ) goods sold at December 31, 2011, under each of the following inventory costing methods (show computations and round to the nearest dollar):

1. Average cost (round average cost per unit to the nearest cent).

2. First in, first out.

3. Last in, first out.

4. Specific identification, assuming that the first sale was selected two fifths from the beginning inventory and three fifths from the purchase of February 20, 2011. Assume that the second sale was selected from the remainder of the beginning inventory, with the balance from the purchase of June 30, 2011.

Aug 29, 2021 | Uncategorized

Evaluating Four Alternative Inventory Methods Based on Income and Cash Flow At the end of January 2012, the records of NewRidge Company showed the following for a particular item that sold at $16 per unit:

|

Transactions

|

Units

|

Amount

|

|

Inventory, January 1, 2012

|

120

|

$960

|

|

Purchase, January 12

|

380

|

3,420

|

|

Purchase, January 26

|

200

|

2,200

|

|

Sale

|

100

|

|

Sale

|

140

|

Required:

1. Assuming the use of a periodic inventory system, prepare a summarized income statement through gross profit for January 2012 under each method of inventory: ( a ) weighted average cost, ( b ) FIFO, ( c ) LIFO, and ( d ) specific identification. For specific identification, assume that the first sale was selected from the beginning inventory and the second sale was selected from the January 12 purchase. Show the inventory computations (including for ending inventory) in detail.

2. Of FIFO and LIFO, which method would result in the higher pretax income? Which would result in the higher EPS?

3. Of FIFO and LIFO, which method would result in the lower income tax expense? Explain, assuming a 30 percent average tax rate.

4. Of FIFO and LIFO, which method would produce the more favorable cash flow? Explain.

Aug 29, 2021 | Uncategorized

Evaluating the LIFO and FIFO Choice When Costs Are Rising and Falling Income is to be evaluated under four different situations as follows:

a. Prices are rising:

(1) Situation A: FIFO is used.

(2) Situation B: LIFO is used.

b. Prices are falling:

(1) Situation C: FIFO is used.

(2) Situation D: LIFO is used.

The basic data common to all four situations are: sales, 510 units for $13,260; beginning inventory, 340 units; purchases, 410 units; ending inventory, 240 units; and operating expenses, $5,000. The following tabulated income statements for each situation have been set up for analytical purposes:

|

PRICES RISING

|

PRICES FALLING

|

|

Situation A FIFO

|

Situation B LIFO

|

Situation C FIFO

|

Situation D LIFO

|

|

Sales revenue

|

$13,260

|

$13,260

|

$13,260

|

$13,260

|

|

Cost of goods sold:

|

|

Beginning inventory

|

3,060

|

?

|

?

|

?

|

|

Purchases

|

4,100

|

?

|

?

|

?

|

|

Goods available for sale

|

7,160

|

?

|

?

|

?

|

|

Ending inventory

|

2,400

|

?

|

?

|

?

|

|

Cost of goods sold

|

4,760

|

?

|

?

|

?

|

|

Gross profit

|

8,500

|

?

|

?

|

?

|

|

Expenses

|

5,000

|

5,000

|

5,000

|

5,000

|

|

Pretax income

|

3,500

|

?

|

?

|

?

|

|

Income tax expense (30%)

|

1,050

|

?

|

?

|

?

|

|

Net income

|

$2,450

|

Required:

1. Complete the preceding tabulation for each situation. In Situations A and B (prices rising), assume the following: beginning inventory, 340 units at $9 = $3,060; purchases, 410 units at $10 = $4,100. In Situations C and D (prices falling), assume the opposite; that is, beginning inventory, 340 units at $10 = $3,400; purchases, 410 units at $9 = $3,690. Use periodic inventory procedures.

2. Analyze the relative effects on pretax income and on net income as demonstrated by requirement (1) when prices are rising and when prices are falling.

3. Analyze the relative effects on the cash position for each situation.

4. Would you recommend FIFO or LIFO? Explain.

Aug 29, 2021 | Uncategorized

Analyzing and Interpreting the Effects of Inventory Errors The income statements for four consecutive years for Colca Company reflected the following summarized amounts:

|

2011

|

2012

|

2013

|

2014

|

|

Sales revenue

|

$60,000

|

$63,000

|

$65,000

|

$68,000

|

|

Cost of goods sold

|

39,000

|

43,000

|

44,000

|

46,000

|

|

Gross profit

|

21,000

|

20,000

|

21,000

|

22,000

|

|

Expenses

|

16,000

|

17,000

|

17,000

|

19,000

|

|

Pretax income

|

$5,000

|

$3,000

|

$4,000

|

$3,000

|

Subsequent to development of these amounts, it has been determined that the physical inventory taken on December 31, 2012, was understated by $2,000.

Required:

1. Recast the income statements to reflect the correct amounts, taking into consideration the inventory error.

2. Compute the gross profit percentage for each year ( a ) before the correction and ( b ) after the correction.

3. What effect would the error have had on the income tax expense, assuming a 30 percent average rate?

Aug 29, 2021 | Uncategorized

Using Financial Reports: Interpreting the Effect of a Change in Accounting for Production Related Costs Dana Holding Corporation designs and manufactures component parts for the vehicular, industrial, and mobile off highway original equipment markets. In a recent annual report, Dana’s inventory note indicated the following:

Dana changed its method of accounting for inventories effective January 1 . . . to include in inventory certain production related costs previously charged to expense. This change in accounting principle resulted in a better matching of costs against related revenues. The effect of this change in accounting increased inventories by $23.0 and net income by $12.9.

Required:

1. Under Dana’s previous accounting method, certain production costs were recognized as expenses on the income statement in the period they were incurred. When will they be recognized under the new accounting method?

2. Explain how including these costs in inventory increased both inventories and net income for the year.

Aug 29, 2021 | Uncategorized

Using Financial Reports: Interpreting Effects of the LIFO/FIFO Choice on Inventory Turnover In its annual report, Caterpillar, Inc., a major manufacturer of farm and construction equipment, reported the following information concerning its inventories:

Inventories are stated at the lower of cost or market. Cost is principally determined using the last in, first out (LIFO) method. The value of inventories on the LIFO basis represented about 70% of total inventories at December 31, 2008, and about 75% of total inventories at December 31, 2007 and 2006.

If the FIFO (first in, first out) method had been in use, inventories would have been $3,183 million, $2,617 million, and $2,403 million higher than reported at December 31, 2008, 2007, and 2006, respectively. On its balance sheet, Caterpillar reported:

|

2008

|

2007

|

2006

|

|

Inventories

|

$8,781

|

$7,204

|

$6,351

|

|

2008

|

2007

|

2006

|

|

Cost of goods sold

|

$38,415

|

$32,626

|

$29,549

|

Required:

As a recently hired financial analyst, you have been asked to analyze the efficiency with which Caterpillar has been managing its inventory and to write a short report. Specifically, you have been asked to compute inventory turnover for 2008 based on FIFO and LIFO and to compare the two ratios with two standards: (1) Caterpillar for the prior year 2007 and (2) its chief competitor, John Deere.

For 2008, John Deere’s inventory turnover was 4.9 based on FIFO and 7.3 based on LIFO. In your report, include:

1. The appropriate ratios computed based on FIFO and LIFO.

2. An explanation of the differences in the ratios across the FIFO and LIFO methods.

3. An explanation of whether the FIFO or LIFO ratios provide a more accurate representation of the companies’ efficiency in use of inventory.

Aug 29, 2021 | Uncategorized

Miga Company and Porter Company both bought a new delivery truck on January 1, 2008. Both companies paid exactly the same cost, $30,000, for their respective vehicles. As of December 31, 2011, the net book value of Miga’s truck was less than Porter Company’s net book value for the same vehicle. Which of the following is an acceptable explanation for the difference in net book value?

a. Miga Company estimated a lower residual value, but both estimated the same useful life and both elected straight line depreciation.

b. Both companies elected straight line depreciation, but Miga Company used a longer estimated life.

c. Because GAAP specifies rigid guidelines regarding the calculation of depreciation, this situation is not possible.

d. Miga Company is using the straight line method of depreciation, and Porter Company is using the double declining balance method of depreciation.

Aug 29, 2021 | Uncategorized

Classifying Long Lived Assets and Related Cost Allocation Concepts – For each of the following long lived assets, indicate its nature and the related cost allocation concept. Use the following symbols:

|

Nature

|

Cost Allocation Concept

|

|

L

|

Land

|

DR

|

Depreciation

|

|

B

|

Building

|

DP

|

Depletion

|

|

E

|

Equipment

|

A

|

Amortization

|

|

NR

|

Natural resource

|

NO

|

No cost allocation

|

|

I

|

Intangible

|

O

|

Other

|

|

O

|

Other

|

|

Asset

|

Nature

|

Cost Allocation

|

Asset

|

Nature

|

Cost Allocation

|

|

(1) Tractors

|

(6) Operating license

|

|

(2) Land in use

|

(7) Production plant

|

|

(3) Timber tract

|

(8) Trademark

|

|

(4) Warehouse

|

(9) Silver mine

|

|

(5) New engine for old

machine

|

|

(10) Land held for sale

|

Aug 29, 2021 | Uncategorized

Identifying Capital and Revenue Expenditures For each of the following items, enter the correct letter to the left to show the type of expenditure. Use the following:

|

Type of Expenditure

|

Transactions

|

|

C Capital expenditure

|

(1) Purchased a patent, $4,300 cash.

|

|

R Revenue expenditure

|

(2) Paid $10,000 for monthly salaries.

|

|

N Neither

|

(3) Paid cash dividends, $20,000.

|

|

(4) Purchased a machine, $7,000; gave a long term note.

|

|

(5) Paid three year insurance premium, $900.

|

|

(6) Paid for routine maintenance, $200, on credit.

|

|

(7) Paid $400 for ordinary repairs.

|

|

(8) Paid $6,000 for extraordinary repairs.

|

|

(9) Paid $20,000 cash for addition to old building.

|

Aug 29, 2021 | Uncategorized

Identifying Asset Impairment For each of the following scenarios, indicate whether an asset has been impaired (Y for yes and N for no) and, if so, the amount of loss that should be recorded.

|

Book Value

|

Estimated

Future Cash Flows

|

Fair

Value

|

Is Asset

Impaired?

|

Amount

of Loss

|

|

a. Machine

|

$15,500

|

$10,000

|

$9,500

|

|

b. Copyright

|

31,000

|

41,000

|

37,900

|

|

c. Factory building

|

58,000

|

29,000

|

27,000

|

|

d. Building

|

227,000

|

227,000

|

200,000

|

Aug 29, 2021 | Uncategorized

Computing Goodwill and Patents Elizabeth Pie Company has been in business for 50 years and has developed a large group of loyal restaurant customers. Giant Bakery Inc. has made an offer to buy Elizabeth Pie Company for $5,000,000. The book value of Elizabeth Pie”s recorded assets and liabilities on the date of the offer is $4,300,000 with a fair value of $4,500,000. Elizabeth Pie also (1) holds a patent for a pie crust fluting machine that the company invented (the patent with a fair value of $300,000 was never recorded by Elizabeth Pie because it was developed internally) and (2) estimates goodwill from loyal customers to be $310,000 (also never recorded by the company). Should Elizabeth Pie Company management accept Giant Bakery”s offer of $5,000,000? If so, compute the amount of goodwill that Giant Bakery should record on the date of the purchase.

Aug 29, 2021 | Uncategorized

Do a detailed benchmarking analysis of the Bookstore’s income statement, five product lines, and financial and operating performance measures, using the Association of Universities and Colleges of Canada Stores’ (AUCC) benchmarking information. Identify performance gaps between the Bookstore results and the AUCC averages and consider possible corrective actions. (12 Marks ~ no page limit) Q2. As required by Tom, Emma must develop a few key related short term goals and related performance measures that could be used in future performance evaluations. What objectives and related performance measures might she consider? Provide specific answers. (3 Marks ~ one page limit) Q3. Assuming all AUCC bookstores are suffering from the same trends and experiencing the same financial difficulties, should Milton be benchmarked against the 25th percentile, the average, or the 75th percentile? Why? Assuming all AUCC bookstores are experiencing superior financial performance and sales growth and Milton is experiencing financial difficulties, is the 25th percentile, the median, or the 75th percentile the best source for benchmarking? Why? (2 Marks ~ half a page limit) Q4. Due to prior superior performance regarding sales of custom materials, assume that Milton has the objective to maintain excellence for this product line. Against which comparison point should this product line be benchmarked (e.g., median, 25th percentile)? Why? (2 Marks ~ half a page limit) Q5. Assume that there is an independent bookstore located near the campus of Milton University that also sells apparel with the Milton logo as well as new and used textbooks. Against which comparison point should these product lines be benchmarked? Why? (2 Marks ~ half a page limit) Q6. Based upon your benchmarking analysis, make appropriate recommendations and decisions for the Milton Bookstore. (5 Marks ~ two page limit)

Aug 29, 2021 | Uncategorized

| The contribution format income statement for Westex, Inc., for its most recent period is given below: |

| |

Total |

Unit |

| Sales |

$ |

994,000 |

$ |

49.70 |

| Variable expenses |

|

596,400 |

|

29.82 |

| |

|

|

|

|

| Contribution margin |

|

397,600 |

|

19.88 |

| Fixed expenses |

|

319,600 |

|

15.98 |

| |

|

|

|

|

| Net operating income |

|

78,000 |

|

3.90 |

| Income taxes @ 40% |

|

31,200 |

|

1.56 |

| |

|

|

|

|

| Net income |

$ |

46,800 |

$ |

2.34 |

| |

|

|

|

|

|

| The company had average operating assets of $508,000 during the period. |

| Required: |

| 1. |

Compute the company%u2019s return on investment (ROI) for the period using the ROI formula stated in terms of margin and turnover. (Round your intermediate calculations and final answers to 2 decimal places.)

|

|

For each of the following questions, indicate whether the margin and turnover will increase, decrease, or remain unchanged as a result of the events described, and then compute the new ROI figure. Consider each question separately, starting in each case from the original ROI computed in (1) above.

|

| 2. |

The company achieves a cost savings of $15,000 per period by using less costly materials. (Round your intermediate calculations and final answers to 2 decimal places.)

|

| 3. |

Using Lean Production, the company is able to reduce the average level of inventory by $100,000. (The released funds are used to pay off bank loans.) (Round your intermediate calculations and final answers to 2 decimal places.)

|

| 4. |

Sales are increased by $198,800; operating assets remain unchanged. (Round your intermediate calculations and final answers to 2 decimal places.)

|

| 5. |

The company issues bonds and uses the proceeds to purchase $129,000 in machinery and equipment at the beginning of the period. Interest on the bonds is $12,000 per period. Sales remain unchanged. The new, more efficient equipment reduces production costs by $4,000 per period. (Round your intermediate calculations and final answers to 2 decimal places.)

|

| 6. |

The company invests $183,000 of cash (received on accounts receivable) in a plot of land that is to be held for possible future use as a plant site. (Round your intermediate calculations and final answers to 2 decimal places.)

|

| 7. |

Obsolete inventory carried on the books at a cost of $20,000 is scrapped and written off as a loss.(Round your intermediate calculations and final answers to 2 decimal places.)

|

Aug 29, 2021 | Uncategorized

Exercise 1 12 The following information relates to David Pande Co. for the year 2014. Owner’s capital, January 1, 2014 $48,456 Advertising expense $ 1,817 Owner’s drawings during 2014 6,057 Rent expense 10,499 Service revenue 64,204 Utilities expense 3,129 Salaries and wages expense 29,780 After analyzing the data, prepare an income statement for the year ending December 31, 2014. DAVID PANDE CO. Income Statement For the Year Ended December 31, 2014 $ $ $ Show List of Accounts After analyzing the data, prepare an owner’s equity statement for the year ending December 31, 2014. (List items that increase owner’s equity first.) DAVID PANDE CO. Owner’s Equity Statement For the Year Ended December 31, 2014 $ : : $ Brief Exercise 2 6 H. Xiao has the following transactions during August of the current year. Aug. 1 Opens an office as a financial advisor, investing $8,236 in cash. 4 Pays insurance in advance for 6 months, $1,590 cash. 16 Receives $3,044 from clients for services performed. 27 Pays secretary $1,334 salary. Journalize the transactions. (Record journal entries in the order presented in the problem. Credit account titles are automatically indented when amount is entered. Do not indent manually.) Date Account Titles and Explanation Debit Credit Brief Exercise 2 10 An inexperienced bookkeeper prepared the following trial balance. HUEWITT COMPANY Trial Balance December 31, 2014 Debit Credit Cash $12,759 Prepaid Insurance $3,133 Accounts Payable 4,592 Unearned Service Revenue 3,792 Owner’s Capital 10,959 Owner’s Drawings 6,092 Service Revenue 27,559 Salaries and Wages Expense 20,559 Rent Expense 4,359 $37,110 $56,694 Prepare a correct trial balance, assuming all account balances are normal. HUEWITT COMPANY Trial Balance December 31, 2014 Debit Credit $ $ Total $ $ Multiple Choice Question 98 Meat Puppets Company purchased equipment for $7,200 on December 1. It is estimated that annual depreciation on the equipment will be $1,800. If financial statements are to be prepared on December 31, the company should make the following adjusting entry: Debit Equipment, $7,200; Credit Accumulated Depreciation, $7,200. Debit Depreciation Expense, $150; Credit Accumulated Depreciation, $150. Debit Depreciation Expense, $1,800; Credit Accumulated Depreciation, $1,800. Debit Depreciation Expense, $5,400; Credit Accumulated Depreciation, $5,400. Multiple Choice Question 104 At December 31, 2014, before any year end adjustments, Murmur Company’s Insurance Expense account had a balance of $2,450 and its Prepaid Insurance account had a balance of $3,800. It was determined that $2,800 of the Prepaid Insurance had expired. The adjusted balance for Insurance Expense for the year would be $5,250. $2,450. $2,800. $3,450. Multiple Choice Question 142 Stone Roses Candies paid employee wages on and through Friday, January 26, and the next payroll will be paid in February. There are three more working days in January (29–31). Employees work 5 days a week and the company pays $1,500 a day in wages. What will be the adjusting entry to accrue wages expense at the end of January? Salaries and Wages Expense 1,500 Salaries and Wages Payable 1,500 No adjusting entry is required Salaries and Wages Expense 7,500 Salaries and Wages Payable 7,500 Salaries and Wages Expense 4,500 Salaries and Wages Payable 4,500

Aug 29, 2021 | Uncategorized

Question: A cost Volume Profit (CVP) income statement is frequently prepared for internal use by management. Describe the features of the CVP that influence make it more useful for management decision making than the traditional income statement that is prepared for external users.

Aug 29, 2021 | Uncategorized

Instructions: 1. Cases will be randomly assigned in class. 2. Research the problem using the online Checkpoint tax research database. 3. Prepare the memorandum following the format of the sample memorandum posted on Blackboard. 4. The memorandum should contain sections. a. Facts . b. Issues c. Conclusion 1. 1 6 sentences. 2. Remember, there is no right or wrong answer. Many of the fact situations may be argued either for or against the taxpayer. d. Discussion Applicable Law 1. Cite Internal Revenue Code sections. 2. Other cites could include Regulations, Revenue Rulings, and court cases. a. Use the PROPER citation forms as shown in Chapter 2. 3. a. Your particular fact situation may or may NOT have applicable Regulations, Revenue Rulings, or court cases. 4. DO try to find all applicable law regarding your fact situation. Analysis 5. In this subsection compare your fact situation to ALL the authorities cited in the “Applicable Law” subsection of this Discussion . 6. IMPORTANT !!! For EVERY authority mentioned in the “Applicable Law” subsection include a COMPLETE analysis of how EACH cited authority relates to the facts of the research problem. 7. Be SPECIFIC and THOROUGH in your comparison. Cite every authority by NAME. COMMON ERRORS ON MEMORANDUM ASSIGNMENTS WHICH WILL RESULT IN POINT DEDUCTIONS 1. Failure to begin “Applicable Law” subsection with cite to a Code section. ALWAYS start with a code section, not the related Regulation. 2. Failure to give a full citation to a Revenue Ruling and, less commonly, a court case. Citation forms are shown in Chapter 2 of the text. 3. Citing to the CCH, RIA, or other tax service. DO NOT cite to these services. Cite to the primary source (i.e., Code, Regulations, Revenue Rulings, etc.). A tax service cannot be cited as an authority when representing your client before the IRS or in court. 4. A weak “Analysis” subsection. Most students do a reasonable job on the “Applicable Law” subsection, but then lose steam when comparing the facts of the particular situation to the “Applicable Law” subsection.

Aug 29, 2021 | Uncategorized

Job Order Cost Accounting Salialailai Ltd manufactures water tanks for different sizes for use by industrial customers. The company uses a job costing system, in which manufacturing overhead is applied on the basis of direct labour hours. The company’s budget for the current year included the following estimates: Budgeted total manufacturing overhead $504,000 Budgeted total direct labour hours 24,000 During March, the company started two production jobs: • Job number ST81, consisting of 76 water tanks (Standard size) • Job number MI45 consisting of 110 water tanks (midi size) The transactions for March are described below: 1,000 square meters of aluminium sheet material were purchased on account for $6,000. • 400 kilograms of aluminium tubing were purchased on account for $5,200 • The following requisitions were filed on 5 March: ? Requisition number 112: 260 square meters of aluminium sheet metal (for job number ST81) @ $5.50 per square meter. ? Requisition number 113: 1,100 kilograms of aluminium tubing (for job number MI45) @ $9 per kilogram ? Requisition number 114: 10 litres of superb glue @ $14 per liter. All aluminium used in production is treated as direct material. Superb glue is an indirect material. • An analysis of labour time sheets revealed the following labour usage for March: ? Direct labour: job number ST81, 850 hours @ $20 per hour ? Direct labour: job number MI45, 950 hours @ $20 per hour ? Indirect labour: general factory clean up, $4,500 ? Indirect labour: factory supervisory salaries, $9,600 • Depreciation of the factory building and equipment during March amounted to $13,000. • Other manufacturing overhead costs incurred in March totalled $9,010. • Sales and administrative expenses for March totalled $13,150. • Job number ST81 was completed in March. • 75% of the water tanks (Standard size) were sold on account during March for $700 each. 19 The March 1st balances in selected accounts are as follows: Cash $11,000 Accounts receivable 20,000 Raw material inventory 50,000 Manufacturing supplies inventory 600 Work in process inventory 89,600 Finished goods inventory 223,000 Accumulated depreciation 99,000 Accounts payable 14,500 Wages payable 8,500 Required: 1. Calculate the company’s predetermined overhead rate for the current year. 2. .Prepare and complete a job cost sheet for Job Number ST81 3. Prepare journal entries (without narration) for March to record the following (Note: Use summary entries where appropriate by combining individual job data): i) the issue of raw material to production ii) the labour costs incurred iii) the manufacturing overhead costs incurred iv) the application of manufacturing overhead to production v) the completion of job(s) in March vi) the sale of job(s) in March 4. Calculate the overapplied or underapplied overhead for March. 5. Prepare a journal entry to close this balance to Cost of goods sold.

Aug 29, 2021 | Uncategorized

Study the information given below and answer the following questions: 4.3.1 Should Scorchers Limited continue to buy the part from the outside supplier or should it produce the part? Motivate your answer with the relevant calculations. (4) 4.3.2 Provide two other factors that are important to this decision. (2)

INFORMATION Scorchers Limited uses a certain part in its manufacturing process that it purchases from an outside supplier at R256 per part including R40 per part for shipping and other purchase related costs. The company estimates that 54 000 of these parts are required next year and is considering making the part Internally. It has sufficient unused capacity to manufacture the 54 000 parts but would need to employ a manager at an annual salary of R432 000 to oversee this production activity. Estimated

production costs (excluding the additional manager’s salary) are as follows: R Direct material 138 Direct labour 60 Variable overheads 30 Fixed overheads (Assumed to be non incremental) 48

Aug 29, 2021 | Uncategorized

Instructions: 1. Cases will be randomly assigned in class. 2. Research the problem using the online Checkpoint tax research database. 3. Prepare the memorandum following the format of the sample memorandum posted on Blackboard. 4. The memorandum should contain sections. a. Facts. b. Issues c. Conclusion 1. 1 6 sentences. 2. Remember, there is no right or wrong answer. Many of the fact situations may be argued either for or against the taxpayer. d. Discussion Applicable Law 1. Cite Internal Revenue Code sections. 2. Other cites could include Regulations, Revenue Rulings, and court cases. a. Use the PROPER citation forms as shown in Chapter 2. 3. a. Your particular fact situation may or may NOT have applicable Regulations, Revenue Rulings, or court cases. 4. DO try to find all applicable law regarding your fact situation. Analysis 5. In this subsection compare your fact situation to ALL the authorities cited in the “Applicable Law” subsection of this Discussion . 6. IMPORTANT !!! For EVERY authority mentioned in the “Applicable Law” subsectioninclude a COMPLETE analysis of how EACH cited authority relates to the facts of the research problem. 7. Be SPECIFIC and THOROUGH in your comparison. Cite every authority by NAME. COMMON ERRORS ON MEMORANDUM ASSIGNMENTS WHICH WILL RESULT IN POINT DEDUCTIONS1. Failure to begin “Applicable Law” subsection with cite to a Code section. ALWAYS start with a codesection, not the related Regulation.2. Failure to give a full citation to a Revenue Ruling and, less commonly, a court case. Citation forms are shown in Chapter 2 of the text.3. Citing to the CCH, RIA, or other tax service. DO NOT cite to these services. Cite to the primary source (i.e., Code, Regulations, Revenue Rulings, etc.). A tax service cannot be cited as anauthority when representing your client before the IRS or in court.4. A weak “Analysis” subsection. Most students do a reasonable job on the “Applicable Law” subsection, but then lose steam when comparing the facts of the particular situation to the “ApplicableLaw” subsection.

Aug 29, 2021 | Uncategorized

Acc 30001/Acc 30008 Accounting Theory Semester 1 2014 Assignment Information Sheet Aligning the Incentives of Managers and Shareholders through Executive Remuneration Individual or Groups of 2 Assignment Due 8.00pm 1st May, 2014 Deegan 4e Question 7.21 p. 328 (adapted) “Within annual reports, companies frequently disclose information about how their managers are rewarded in terms of the components of their management compensation plans. For example, within IAS 24 (and AASB 124 within Australia) there is a requirement that information about the components of rewards paid to key management personnel be disclosed within a company’s annual report.” Required: a) Select two large companies listed on the Australian Securities Exchange (ASX) that issue share options as part of their remuneration for key managerial personnel. Use the financial year 2013 annual reports for listed companies to select two such companies, but generally companies within the S&P ASX All Ordinaries Index use stock options as a remuneration mechanism. 2 You are required to explain in a report for the Chief Accountant of the Australian Securities & Investments Commission how the respective components of the remuneration could be expected to align the interests of the managers with those of the owners and to minimise the contracting costs of the organisation. In your report you are expected to draw on (not necessarily in the numbered order): 1) the chosen annual reports 2) at least six quality*, scholarly articles from JOURNALS that appear in the Australian Business Deans’ Council (2013) ranking of journals – Business Source Complete (Ebscohost) is a Library database that hosts scholarly journal articles. 3) media reports of the workings in practise of the Corporations Amendment (Improving Accountability on Director and Executive Remuneration) Act 2011.No. 42, which provided shareholders with a ‘say on pay’ and which may result in ‘first strike’ or ‘second strike’ votes by shareholders. Factiva is a Library database that hosts newspapers). Note: Research for and writing of the assignment can be commenced after the first tutorial. Positive accounting theory is covered specifically in Lecture 6. Executive remuneration is covered specifically in Chapter 7 (pages 291 301) of the prescribed text. Some students find reading scholarly journal articles very difficult. YouTube clips that help with this can be found on Blackboard under ‘Assignments’. *The quality of journals can be assessed by reference to the Australian Council of Business Deans (ABDC) 2013 journal rankings (A*, A, B, C in order of declining quality) available http://www.abdc.edu.au/journalreview l Learning outcomes addressed by the assignment. The assignment is designed to provide you with the opportunity to develop the following learning outcomes: 1 with regard to your accounting theory knowledge, the assignment provides you with the opportunity to develop your understanding of positive accounting theory and, in 3 particular, agency or costly contracting theory and its application to executive remuneration. 2. with respect to generic skills, the assignment provides you with the opportunity to develop your ability to research and analyse complex issues, to formulate well reasoned and coherent arguments and to reach well considered conclusions, and to develop your written communication skills, including the conventions of referencing at university. You are to aspire to the highest standard of work with respect to both the content and presentation of the Report. The Harvard referencing system is to be used as applied by the American Accounting Association’s The Accounting Review an A* journal (ABDC rankings). Marks will be deducted where the Harvard system is not used appropriately. Please note that Wikipedia is not an appropriate source to reference for an academic Report such as this. The Library holds sessions on referencing technique and provides guidelines at http://www.swinburne.edu.au/lib/researchhelp/harvard_style l. LODGEMENT: You must submit your assignment via the Turnitin facility available on Blackboard no later than 8.00pm 1st May, 2014. Students must also keep an electronic or photocopied version of their assignment for evidentiary purposes. The file name should be Surname1_Surname2 (in the case of a submission by two students). MAXIMUM MARKS: 20 Marks toward the final assessment. The assignment will be marked out of 100. The rubric for marking is in the Unit Outline. Assignments will be marked to the same standard regardless of whether one or two students are involved in the submission. When working in pairs, students are expected to contribute equally. On this basis each student responsible for a submission is provided the same mark. Where equal contributions are not forthcoming and this cannot be resolved by the students themselves, the Convenor should be informed in writing. WORD COUNT: the body of the Report should not exceed 1500 words (+/ 10 per cent) (excluding title page, references and executive summary but including footnotes, endnotes and appendices). Please provide a word count on the cover sheet. 4 FORMAT A report format is required for this assignment. In a report, the Executive Summary should provide an overview of the whole report, including any recommendations. This is a ‘thinking’ assignment and what is expected is the personal view of individual students’ based on research and the evidence that has been sourced. Further, an assignment which presents more quotes than constructive analysis and argument may be heavily penalised. SUGGESTED REPORT STRUCTURE 1. Title Page 2. Contents Page 3. Executive Summary (which provides an overview of the whole report) 4. Introduction and Purpose 5. Responses to specific task using appropriate headings and sub headings 6. Conclusion 7. References This assignment is an important assessment component of this Unit and as such the assignment must be properly researched and professionally presented. The assignment should also: • Be all your own (individual submissions) or your group’s (pairs) work • Be word processed (printed), and have 1.5 spacing for clarity; a high standard of presentation is expected • Have the cover sheet with all relevant details, including: student name, student number, tutorial time & tutor’s name Unit name and code date of submission • Contain correct referencing, using the Harvard system. • Include a list of references (alphabetical by first author’s surname) adequately referencing your sources (in text references should only refer to the surname of the author/authors and the year of the publication). 5 Students are reminded to review the University policy on plagiarism. The University uses the Turnitin tool. This is an effective tool to reduce plagiarism. Students should self check their assignments prior to final submission. Documentation on the use of this tool will be posted on Blackboard. Please ensure that you use only the Draft option to check your work. This is a matching and not a punitive tool. The default setting allows every student to check draft submissions, but you should be aware that the closer to the deadline you use Turnitin, the longer it may take to receive a report. Upon receiving feedback from Turnitin, you should amend your assignment to ensure that it is “Plagiarism Safe” before

Aug 29, 2021 | Uncategorized

Elctro Company manufactures an innovative automobile transmission for electric cars. Management predicts that ending finished goods inventory for the 1st quarter will be 80,180 units. The following unit sales of the transmissions are expected during the rest of the year: 2nd quarter 211,000 units, 3rd quarter 497,000 units and 4th quarter 239,000 units. Company policy calls for the endinf finished goods inventory of a quarter to equal 38% of the next quarter’s budgeted sales. (Ending inventory for the 1st quarter does not comply with company policy.) Each transmission requires 0.57 pouns of a key raw material. Electro Company aims to end each quarter with an ending inventory of dorect materials equal to 38% of next quarter’s budgeted materials requirements. Direct materials cost $169 per unit.Prepare a direct materials budger for the 2ndquarterwith the following:2nd quarter’s budgeted production units is 391,680 units, materials needed for production pounds is 182,218 lbs. Budgeted beginning inventory is 69,243 lbs. What is Budgeted ending inventory lbs and materials price per lb? $296 per lbs is not correct

Aug 29, 2021 | Uncategorized

a)Contingency theory has frequently been used to explain variations in the functioning of organizations.It has been criticized on a number of grounds, including whether sufficient attention has been given to people and culture.

Requirement

Explain and discuss from a management control perspective, the criticism that contingency theory pays insufficient attention to the people in organizations and to organizational culture.

(b)Some organizations have long standing practices of promoting from existing staff, as a consequence of which they rarely recruit outsiders to any senior position.Staff turnover is vey low.Other organizations have frequent management and structural changes, and often recruit senior managers from outside the organization.

Requirement

Explain the differences in control systems and approaches to management control hat could be expected with these alternative practices.

Question 3

Describe the contingency theory of management accounting and

discuss the relationship between various contingent factors and

features of the management accounting system.

Aug 29, 2021 | Uncategorized

|

4. On the basis of the following data for Grant co. for 2010 and the preceding year ended December 31,2009, prepare a statement of cash flows. Use the indirect method of reporting cash flows from operating activities. Assume the equipment costing $125,000 was purchased for cash and equipment costing $85,000 with accumulated depreciation of $65,000 was sold for $15,00: that the stock was issued for cash: and that the only entries in the retained earnings account were net income of $56,000 and cash dividends declared of $18,000

2010 / 2009

Cash$90,000 / $78,000

Accounts Receivable $78,000 / $85,000

Inventories $106,500 / $90,000

Equipment $410,000 / $370,000

Accum. Depreciation $150,000 / $158,000

TOTAL$534,500 / $465,000

Accounts Payable$53,500 / $55,000

Cash Dividends Payable $5,000 / $4,000

Common Stock, $10 par$200,000 / $170,000

Paid in capital excess par $62,000 / 60,000

Retained Earnings $214,000 / $176,000

TOTAL$534,000 / $465,000

|

Aug 29, 2021 | Uncategorized

Use the following table of states of the economy and stock returns to answer the review problems:

|

|

|

Security Returns

if State Occurs

|

|

State of

|

Probability of State

|

Roten

|

Bradley

|

|

Economy

|

of Economy

|

|

|

|

Bust

|

0.4

|

10%

|

30%

|

|

Boom

|

0.6

|

40

|

10

|

|

|

1

|

|

|

1. Expected Returns Calculate the expected returns for Roten and Bradley.

2. Standard Deviations Calculate the standard deviations for Roten and Bradley.

3. Portfolio Expected Returns Calculate the expected return on a portfolio of 50 percent Roten and 50 percent Bradley.

4. Portfolio Volatility Calculate the volatility of a portfolio of 50 percent Roten and 50 percent Bradley.

Aug 29, 2021 | Uncategorized

We calculate the expected return as follows:

|

|

|

Roten

|

Bradley

|

|

(1)

|

(2)

|

(3)

|

(4)

|

(5)

|

(6)

|

|

State of

|

Probability of State of

|

Return if

|

Product

|

Return if

|

Product

|

|

Economy

|

Economy

|

State

|

(2) × (3)

|

State

|

(2) × (5)

|

|

Bust

|

0.4

|

Occurs

|

|

Occurs

|

|

|

Boom

|

0.6

|

10%

|

0.04

|

30%

|

0.12

|

|

|

|

40%

|

0.24

|

10%

|

0.06

|

|

|

|

E(R) =

|

20%

|